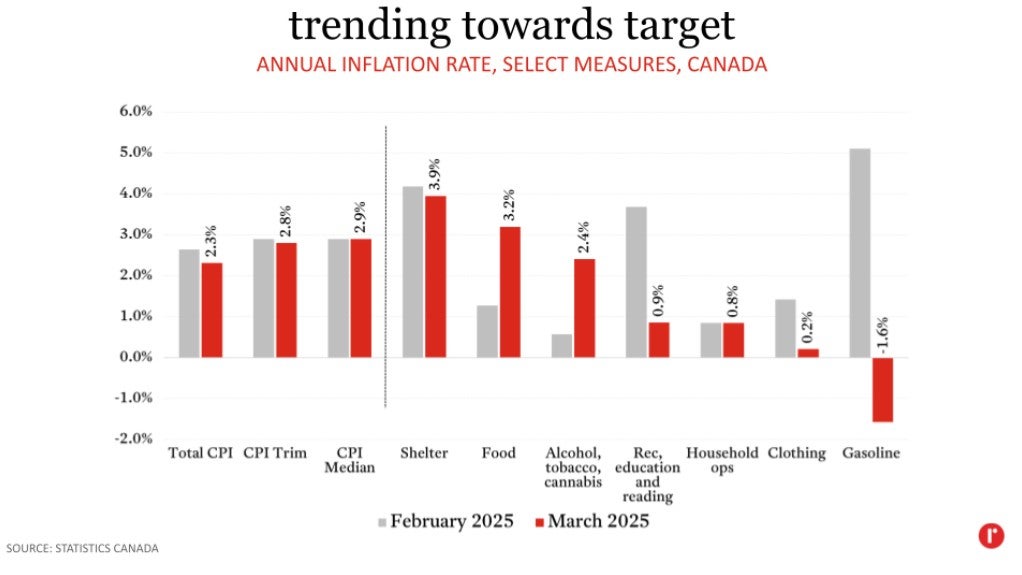

Much of the decrease last month can be attributed to base-year effects on gasoline. Prices at the pump eased in March, in contrast to the same time last year when they were rising rapidly, resulting in an annual decline in the gasoline component of the CPI. This outweighed increases in two other components of the CPI that were driven by the end of the GST holiday in mid-February: food (specifically food from restaurants) and alcoholic beverages, tobacco, and cannabis, which saw their annual rates of inflation increase to 3.2% and 2.4%, respectively.

Because the decline in headline inflation was driven primarily by gasoline, which is volatile, core measures of inflation (which strip out the most volatile elements) were relatively unchanged last month. The Bank of Canada’s preferred measures, CPI Trim (2.8%) and CPI Median (2.9%), remained elevated relative to the overall rate of inflation, suggesting there are some underlying price pressures that the Bank will take note of.

With inflation once again cooling near target and a relatively soft jobs data release for March, the possibility of another interest rate reduction from the Bank of Canada on April 16th is open, although the outcome is far from certain. Looking ahead, the consumer carbon tax was removed in April, and with additional base-year effects, gasoline inflation will decline further next month. The Bank will also have to weigh the latest data against the backdrop of US tariffs on Canada, Canadian counter-tariffs on the US, as well as the potential impact on demand for Canadian exports, given that the US has imposed tariffs on virtually every country on earth.

The near-daily changes to the tariffs and their rates are only adding to the uncertainty about the impacts of these policies. In its statement on March 12th, the Bank noted, “Monetary policy cannot offset the impacts of a trade war. What it can and must do is ensure that higher prices do not lead to ongoing inflation.” Regardless of whether the Bank opts to lower or hold its policy rate on April 16th, expect it to proceed cautiously through the rest of 2025 as it assesses and reassesses each new policy with an eye to keeping inflation in check.

With inflation once again cooling near target and a relatively soft jobs data release for March, the possibility of another interest rate reduction from the Bank of Canada on April 16th is open, although the outcome is far from certain. Looking ahead, the consumer carbon tax was removed in April, and with additional base-year effects, gasoline inflation will decline further next month. The Bank will also have to weigh the latest data against the backdrop of US tariffs on Canada, Canadian counter-tariffs on the US, as well as the potential impact on demand for Canadian exports, given that the US has imposed tariffs on virtually every country on earth.

The near-daily changes to the tariffs and their rates are only adding to the uncertainty about the impacts of these policies. In its statement on March 12th, the Bank noted, “Monetary policy cannot offset the impacts of a trade war. What it can and must do is ensure that higher prices do not lead to ongoing inflation.” Regardless of whether the Bank opts to lower or hold its policy rate on April 16th, expect it to proceed cautiously through the rest of 2025 as it assesses and reassesses each new policy with an eye to keeping inflation in check.